|

| Not a hawk in sight |

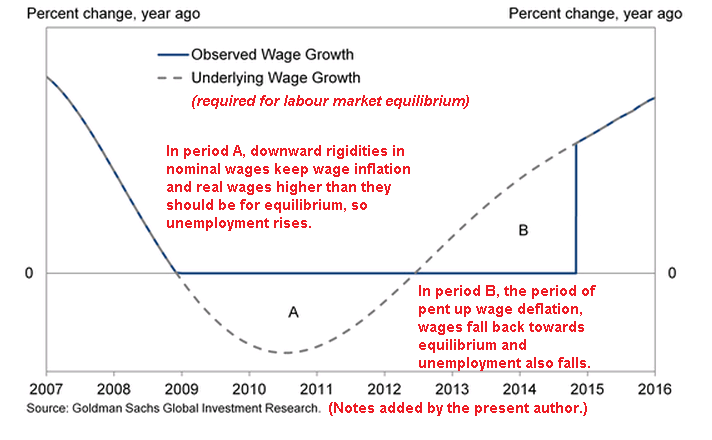

A chart provide by Gavyn Davies at the FT summaries the model for "pent up wage deflation" much more coherently than I can explain.

The problem for the Fed and other central bankers is that the stickiness of wages is not uniform (the single line on GD's chart hides a range of possibilities) . In the public sector wages are very sticky and labour cost can only be reduced by lay-offs and natural wastage (not replacing retirees). In fact in the UK public sector incomes rose in the years 2009 - 2011, whist the private sector was in free fall. As an example of private sector wage unstickiness - in a partnership wages will always stay in line with performance as partners share profits, earning in Law firms fell heavily during the Great Recession and are still falling. Also in industries where earnings are impacted by variable commissions and bonuses wages are not at all sticky. As the chart below (from the Daily telegraph) illustrates wages are any thing but sticky in the UK's private sector.

The problem for central bankers is that the statistics they use for policy decisions are blunt national averages, which mask the actual behaviour of the economy. It is quite likely that in the US and the UK the productive economy has got some wage inflation but this is hidden by static wages in the public sector, which are still frozen to ensure that we can lower deficits in our public finances. In other sectors that are exposed to global competition (legal services) there will also be deflation - but these examples are not a function of demand shortfall and will not be corrected with negative real interest rates.

So we have the unhelpful situation that interest rates and other monetary policies are being judged against the unproductive economy rather than being targeted at the real economy that generates real jobs, wealth and growth. We are probably in a situation where the private sectors needs some tighten but this cannot happen until governments can afford to pay civil servants higher wages for doing the same work; given the state if public finances this won't be any time soon.

The big question is whether we should be making economic decisions based on the whole economy or whether we should focus on the parts of the economy we want to grow. If we need to shrink the State why should we be worried if wages are falling in the public sector. Anyway as we have already discussed interest rates will have little or no impact on public sector employment levels.

However, if we want our growth industries to remain competitive we must be alert to wage inflation in our productive economy an act appropriately.

No comments:

Post a Comment